By Geraint John

Restrictions on global free trade and supply chain relationships are flying around like Chinese “spy” balloons over North America were just a few weeks ago.

Last month, China slapped sanctions on U.S. defense giants Lockheed Martin and Raytheon, ostensibly because of their arms sales to Taiwan. But the move was widely interpreted as retaliation for the U.S. government’s decision a few days earlier to blacklist six Chinese companies it accuses of being involved in China’s surveillance-balloon program.

So far this month, the American military has shot down one high-altitude Chinese balloon and three unidentified objects over U.S. and Canadian airspace. China denies U.S. government claims that the balloon was spying on sensitive installations. Their government claims it was used purely for weather monitoring.

Regardless of whose version is true, these tit-for-tit sanctions are part of an escalating technology war between the U.S. and its allies and China that threatens to blow apart the international trading system as we know it.

Global Trade Restrictions Have Increased Sharply

As with geopolitical tensions, trade restrictions on goods, services and foreign investment have increased sharply in recent years. From 2018, when the Trump administration imposed tariffs of up to 25% on many Chinese imports, to December 2022, the number of worldwide restrictions more than doubled to around 2,500, according to data from the International Monetary Fund and Global Trade Alert.

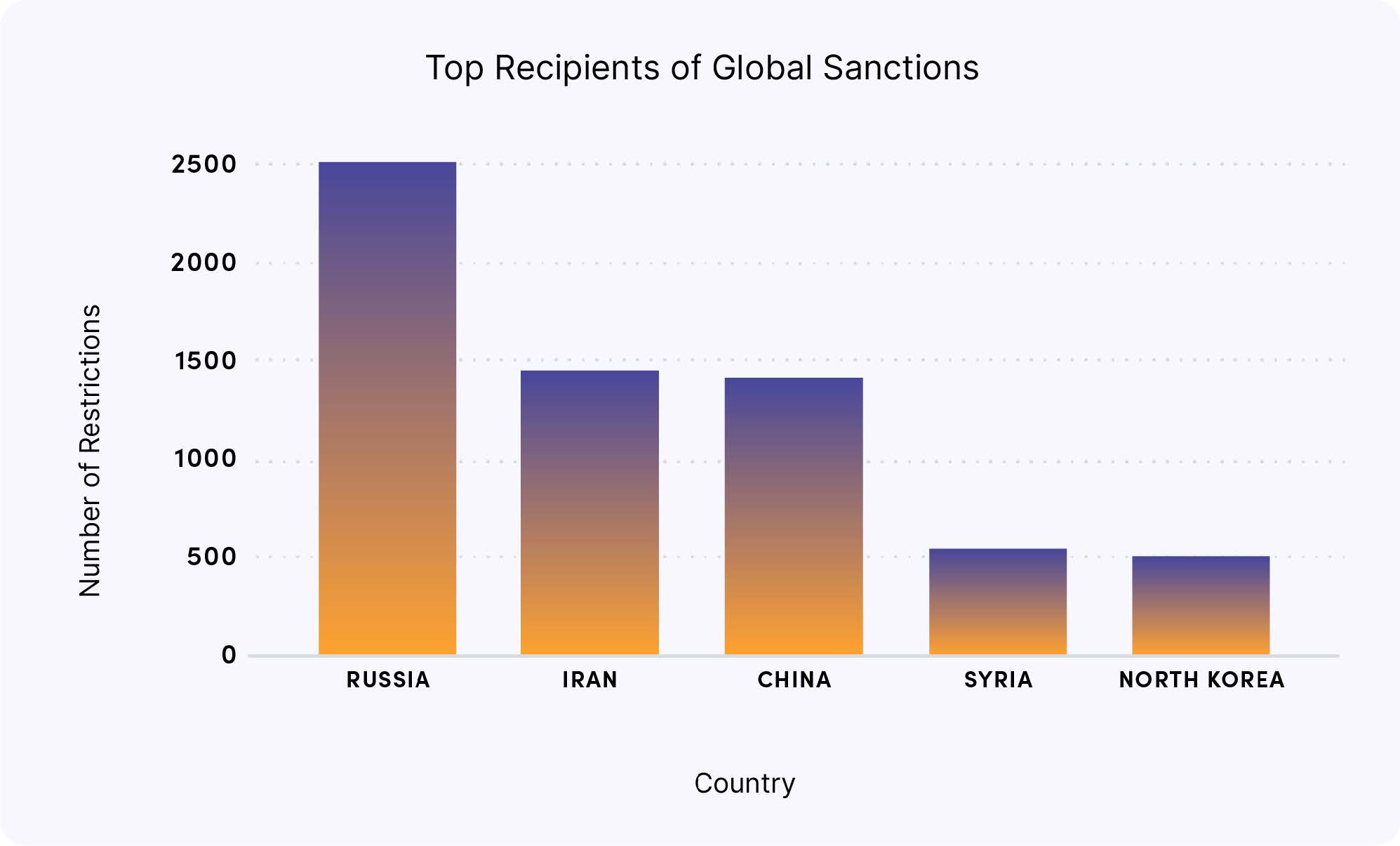

A new Interos white paper reveals that Russia displaced China as the most targeted country for restrictions last year, following its invasion of Ukraine. More than 1,100 restrictions were imposed on Russian entities in 2022 – almost six times more than China.

Russia is also well ahead of Iran and China in terms of the total number of restrictions imposed by other nations since 1981 (see chart).

On the opposite side, the U.S. dwarfs other countries in the number of restrictions it issues (around 8,000 during the past 40 years). And it has dozens of restricted entity lists across different government departments and industry sectors.

Prominent examples include:

- The Department of Commerce’s Entity List, which sets out export licensing requirements for hundreds of foreign-owned businesses.

- Sections 889 and 5949 of the National Defense Authorization Act banning the use of certain Chinese products and services for military purposes.

- The Department of Homeland Security’s UFLPA Entity List for the Uyghur Forced Labor Prevention Act, which bars imports of tainted products from the Xinjiang region of China.

Keeping up to date with the ever-expanding list of prohibited firms and ensuring your organization doesn’t fall foul of new trade rules has become a more complex task. Which is why restrictions risk is one of the six risk factors captured and updated continually in Interos’ Resilience platform.

Implications for Global Supply Chains in Light of Trade Sanctions Against China

Standing back from the detail of these multiple lists and regulations, it’s important to consider the broader implications of the spiraling number of restrictions on international supply chains.

During the past couple of years, the U.S. has implemented progressively tighter and more far-reaching rules around the sourcing of Chinese components and sales of American semiconductors and chip-making equipment to Huawei and other Chinese tech firms.

This is having a dramatic impact on the ability of these companies to scale up production and manufacture products.

Last month, China’s semiconductor industry body issued a strongly worded statement condemning action by the U.S., Japan, and the Netherlands to deny its members vital equipment.

Such measures would “destroy the global semiconductor ecosystem”, it claimed.

Trade Restrictions on China Signal Broader Supply Chain Trend

While complaining loudly and portraying itself as the defender of free trade and globalization – as it did at the World Economic Forum’s meeting of political and business leaders in Davos in January — China is also flexing its trade-restriction muscles.

It has, for example, threatened to stop the export of solar panel manufacturing equipment to the U.S. China dominates the supply chain for this crucial clean-energy technology and could — in a mirror image of its own semiconductor woes — impede American efforts to beef up its domestic solar industry.

Although trade between China and the U.S. grew strongly last year, economists and other critics argue that protectionism, “decoupling,” and politically led moves towards “friend-shoring” (or “ally-shoring”) could have negative consequences for the global economy and supply chains in the years ahead.

These include higher prices, lower efficiency, less innovation, wasted public money through ineffective subsidies and industrial policies, and diminished levels of resilience.

As FT columnist Martin Wolf cautioned in a piece on the “new interventionism” last month: “Fragmentation is very easy to start. But it will be hard to control and even harder to reverse.”

Get more information on trade restrictions, sanctions, regulatory changes and their impact on the global supply chain by reading our latest white paper – the Red Tape Revolution.